On October 10, SHFE Copper futures warehouse receipt was 3,729 tonnes, unchanged from the previous trading dayand in the past week; the cumulative increase in the past month was 281 tonnes, an increase of 8.15%.

During National Day holiday period, LME copper first rose and then fell, finally slightly decreased to $7,462/tonne. The US dollar was boosted by the higher-than-expected US NFP and a higher probability of a further substantial rate hike in November. The risk of a recession also increased, caused the copper price under pressure to fall. Crude oil prices boosted by production cuts, which have hurt downward of inflation and effectively raised the possibility of recession in the future. The conflict between Russia and Ukraine is at risk of escalation, leading to greater pressure on the European economy.

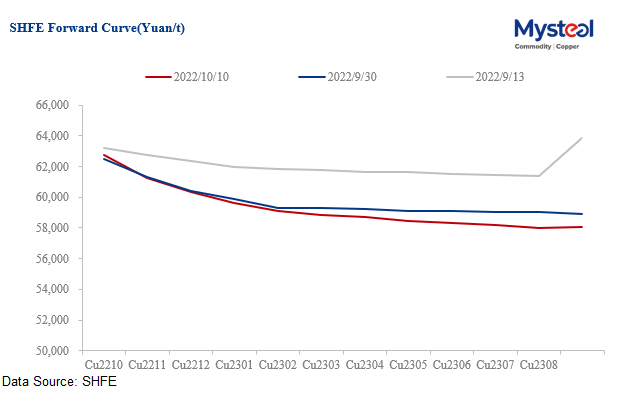

During the holiday period, LME copper inventories rose by about 5,000 tonnes, and the spot premium also fell to $50/tonne. China's copper supply is tight and social inventories are historically low, curbing the decline in copper prices. Whether the social inventory can usher in the inflection point after the holiday still needs to be focused on.

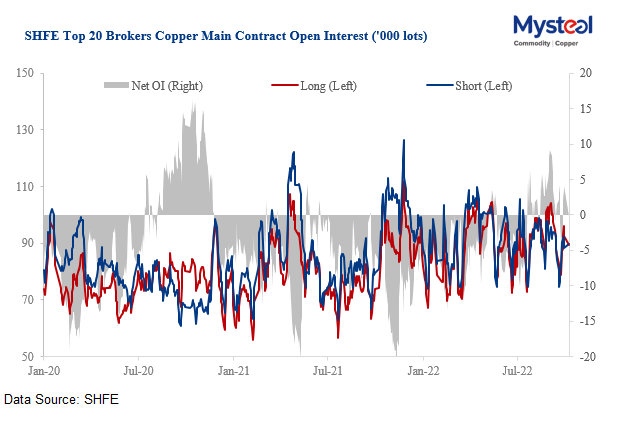

Overall, the current macro-outlook is still not optimistic, lacks conditions to promote copper prices upward. The margin of safety of short orders is relatively better. It is recommended continue to hold short orders or take advantage of the high price to increase short positions.

For queries and more information/data/reports access, please contact Paula Xu at xuzhongping@mysteel.com