On October 12, SHFE Copper futures warehouse receipt was 9,668 tonnes, 5,112 tonnes more than the previous trading day; the cumulative increase in the past week was 5,939 tonnes, an increase of 159.27%; the cumulative increase in the past month was 6,220 tonnes, an increase of 180.39%.

US NFP data were strong. The Fed's hawkish toughness hit market risk sentiment and kept the dollar index strong. Another 75-basis point rate hike is expected at the Fed's November meeting, which leaves expectations for future global economic growth rates to remain pessimistic and depressing copper demand.

The increase in copper concentrate imports led to a rise in copper concentrate TC. As power shortages in China are eased, therefore, driven by profits, smelters are ramping up production. But the tightening in blister copper supplies could lead to actual production falling short of expected. It is still the traditional peak season currently, coupled with the historically low levels of copper inventories, the overall premium will remain high. However, the recent rapid rise in future back has also led to buyers reduce purchasing to avoid the possible risk of short squeeze, which reflects a rebound in inventory.

Overall, the current macro and fundamental outlooks are still not optimistic, lacking factors to promote copper prices upward. It is recommended to hold short position or increase short position when price rebounds.

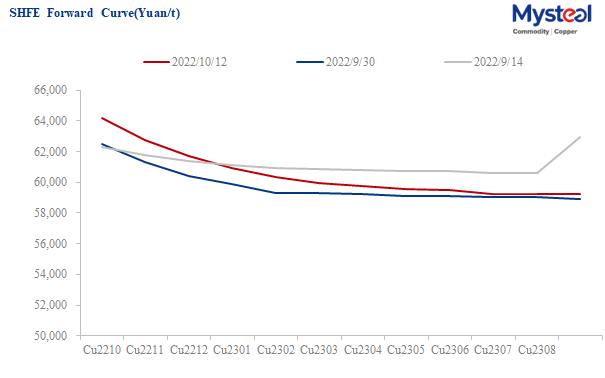

Data Source: SHFE

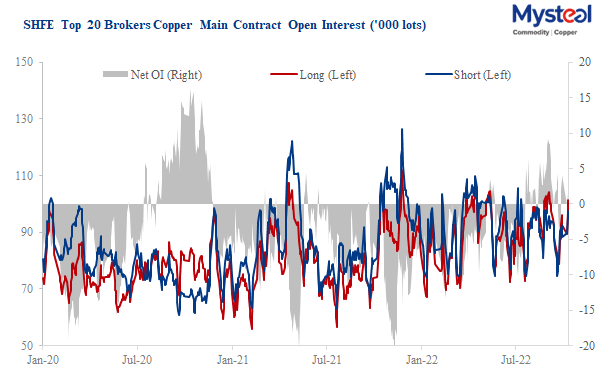

Data Source: SHFE

For queries and more information/data/reports access, please contact Paula Xu at xuzhongping@mysteel.com