On October 14, SHFE Copper futures warehouse receipt was 25,588 tonnes, 11,495 tonnes more than the previous trading day; the cumulative increase in the past week was 21,859 tonnes, an increase of 586.19%; the cumulative increase in the past month was 22,364 tonnes, an increase of 693.67%.

The US core CPI was recorded at an annualized rate of 6.6% in September, beat expectations of 6.5% and the highest since August 1982. For now, high inflation is unlikely to change in the short term. Market expectations of a continued Fed tightening of monetary policy have been strengthened again.

Demand for copper concentrate at smelters remained weak. However, TCs still remained high at Yuan 84/tonne. CSPT held an online meeting to set a spot TC guidance price for copper concentrate at $93/dry tonne in the fourth quarter of 2022. In September and October, smelter overhaul arrangements became more frequent, involving a total capacity of more than 1.6 million tonnes. But there is also the expectation of new capacity for smelters of 400,000 tonnes in central China. The possibility of increased imported copper supply in the future is also further improved. Overall, the likelihood of a gradual easing of supply is conceivable.

Copper prices are still more bearish under macro recession pressure and weaker fundamentals. The copper price center of gravity is expected to gradually move down in large fluctuations in October. It is recommended to continue to hold short orders, while buy deep virtual put options to protect tail risk.

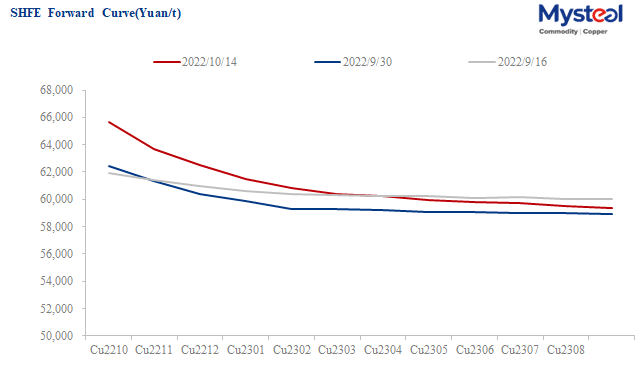

Data source: SHFE

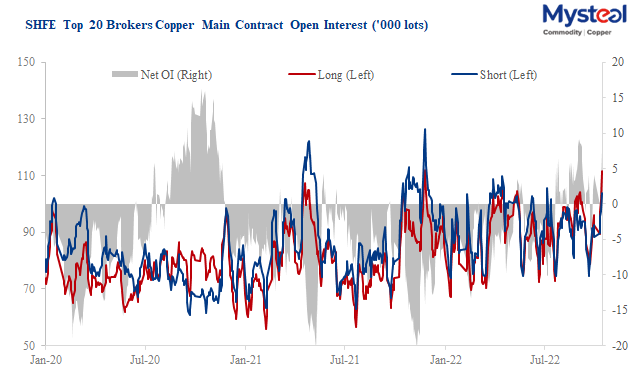

Data source: SHFE

For queries and more information/data/reports access, please contact Paula Xu at xuzhongping@mysteel.com