On October 13, SHFE Copper futures warehouse receipt was 14,093 tonnes, 4,425 tonnes more than the previous trading day; the cumulative increase in the past week was 10,364 tonnes, an increase of 277.93%; the cumulative increase in the past month was 10,869 tonnes, an increase of 337.13%.

LME copper inventory fell 125 tonnes to 145,400 tonnes on October 13. China's Social financing scale increased by 3,530 billion yuan in September, compared with 2,432.2 billion yuan previously. China's M2 rose 12.1% year on year in September, compared with 12.2% previously. New yuan-denominated loans reached 2.47 trillion yuan in September, compared with 1.25 trillion yuan previously. The rebound in China's macroeconomic data has been partially supportive of copper prices.

The latest US NFP is again better than expected, the unemployment rate has backed to a 53-year low, and the wage-inflation spiral continues. All this means the Fed still needs to raise interest rates further to cool the overheated economy. Cleveland Fed President Loretta Mester said on Tuesday that the central bank cannot be complacent and still needs to keep raising interest rates as it tries to fight the worst inflation in decades.

China is halfway through its peak demand season of copper. There is a risk that consumption will weaken continuously. With the recovering of global copper inventories, the short squeeze may be hard to sustain.

Copper prices are still more bearish under macro recession pressure and weaker fundamentals. The copper price center of gravity is expected to gradually move down in large fluctuations in October. It is recommended to continue to hold short orders, while buy deep virtual put options to protect tail risk.

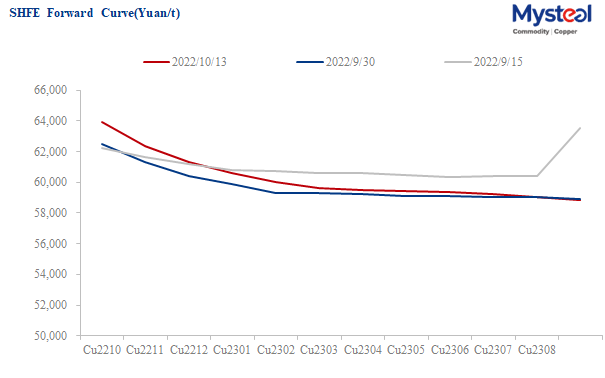

Data Source: SHFE

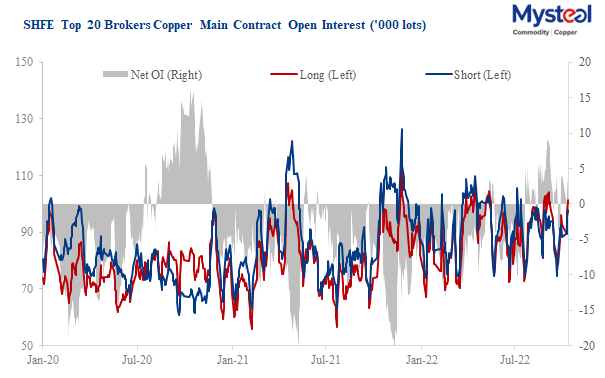

Data Source: SHFE

For queries and more information/data/reports access, please contact Paula Xu at xuzhongping@mysteel.com