On October 17, SHFE Copper futures warehouse receipt was 72,612 tonnes, 47,024 tonnes more than the previous trading day; the cumulative increase in the past week was 68,883 tonnes, an increase of 1847.22%; the cumulative increase in the past month was 63,061 tonnes, an increase of 660.26%.

Based on the performance of the US CPI data released last Thursday, copper prices showed a "profits made" and a short-term rebound, indicating a wide divergence between bulls and shorts. But expectations of a recession are not over, limiting the scope for a long-term rebound. US inflation data for September came above consensus estimates again, further reinforcing expectations that the Fed will remain hawkish. Recession expectations remain high in Europe and the US. The International Monetary Fund cut its forecast for global GDP in 2023 to 2.7%.

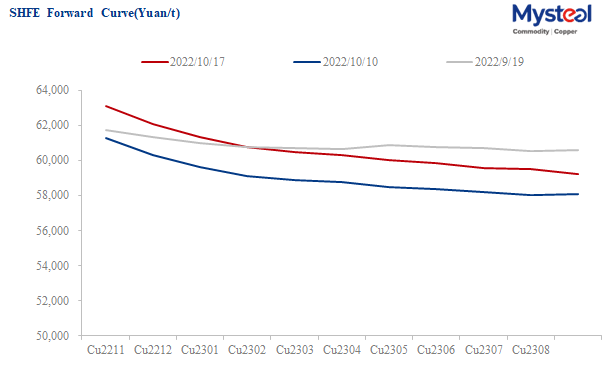

China's domestic epidemic has been volatile, but the impact on futures prices is waning. The supply ramps up gradually. But during the peak demand season, low inventories may continue for a while, supporting the big-back contract structure. Manufacturing demand is at a seasonal peak in October, so there will be no significant weakening in fundamentals in the short term. It is even possible to see continued improvement in demand. Inventories of three major exchanges and in the free trade zone are still low, providing support for the price. But signs of a rebound in China's copper inventories have emerged, and its sustainability remains to be seen.

Overall, the copper price will rebound periodically in the short term while having a weak trend in the fourth quarter. It is still recommended to short at a high price while buying deep virtual put options to protect the tail.

Data Source: SHFE

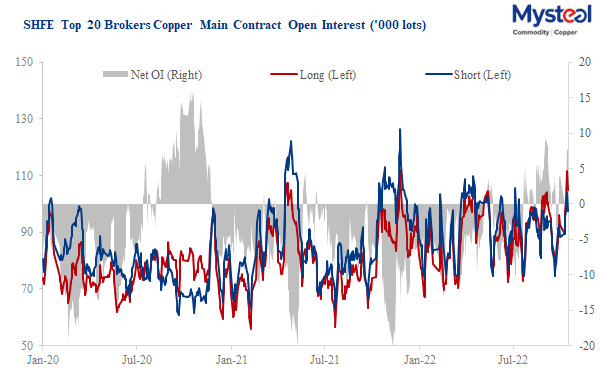

Data source: SHFE

For queries and more information/data/reports access, please contact Paula Xu at xuzhongping@mysteel.com