The Shanghai Futures Exchange's (SHFE) warehouse warrants for copper futures fell 12,783 tonnes day on day to 52,287 tonnes on October 21, leading to a week-on-week spike of 26,699 tonnes or 104.34%, and a surge of 44,341 tonnes or 558.03% month on month.

Spot inventories of copper remained historically low. Geopolitical risks have also not subsided, which is expected to cause range-bound of copper prices in the short term. But it is difficult to reverse the long-term downward trend. With the approaching off-season, copper prices are expected to weaken again due to a reversal in supply and demand patterns and the beginning of inventory accumulation.

From the performance of copper prices in the past 30 years, it did not show weakness immediately after the Fed raised interest rates but mostly showed strong performance. However, copper prices are likely to fall significantly in the recession phase. The market's fear is not raising interest rates itself, but the prospect of a recession triggered by a sharp hike in a gloomy economic scenario.

Some overseas consumers are boycotting Russian copper, which has accelerated the concentrated inflow of LME copper before the sanction, resulting in Russian copper accounting for more than 60% of existing LME inventories.

With sanctions in place, copper destined for Europe and the US is likely to be shipped to China, creating a supply mismatch. Copper prices will continue to be depressed in the long term as supply will recover and the global economy enters recession. SHFE copper is more strongly influenced by the exchange rate. Under the weak situation of CNY, SHFE copper is expected to continue to show more resistance to decline than LME copper.

Copper prices are expected to be bearish in the fourth quarter amid rising global stagflation concerns and monetary tightening. The pressure level in SHFE copper is Yuan 65,000-66,000/tonne, and the bottom level is Yuan 56,000-58,000/tonne. There is strong support around the 90-percentile copper cost in the extreme case, which is Yuan 53,000/tonne. It is still recommended to mainly short at a high price.

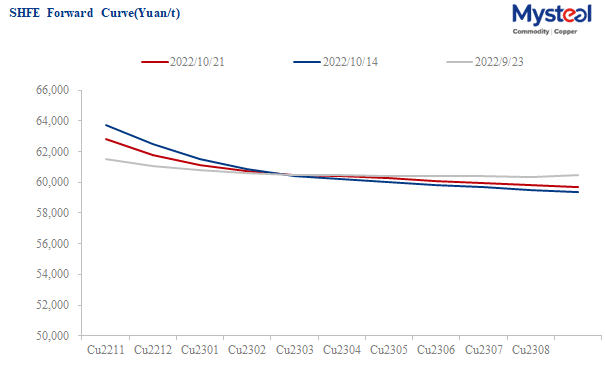

Data Source: SHFE

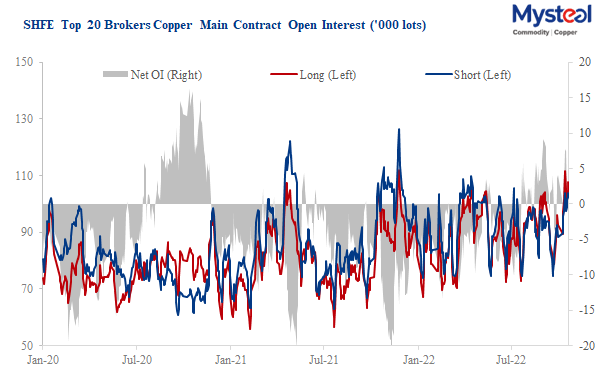

Data Source: SHFE

For queries and more information/data/reports access, please contact Paula Xu at xuzhongping@mysteel.com