On September 29, SHFE Copper futures warehouse receipt was 3,729 tonnes, 275 tonnes less than the previous trading day; the cumulative decrease in the past week was 2,957 tonnes, a decrease of 44.23%; the cumulative decline in the past month was 124 tonnes, a decrease of 3.22%.

The US dollar index rally paused; copper prices rebounded significantly. However, the logic of US dollar strength has not changed, and may just enter the adjustment phase after the previous surge. First, the inflation data has exceeded expectations and the Fed is pessimistic about the pace of interest rate hikes. Second, the US economic data has been relatively strong compared with Europe. The geopolitical risks of Russia and Ukraine have limited impact on the market, and the possibility of further escalation is not high. The overall macro level is still gradually digesting the impact of the Fed's rate hike, but the impact of the liquidity squeeze on the market will not fade in the short term.

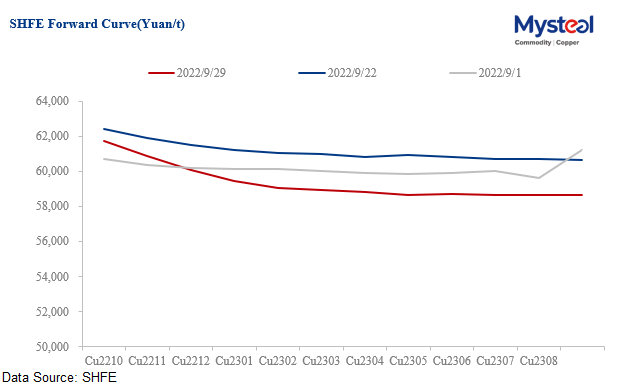

Macro pressure has increased, copper prices may remain weak. But the big back is likely to persist as global inventories remain low. It is recommended to continue to observe the support strength around Yuan 60,000/tonne of refined copper.

The current copper price drop range is larger, and the market sentiment is pessimistic. It is recommended to appropriately reduce the short positions. In view of the medium and long term is still in the recession cycle, it is recommended to short at every high point. Avoid too much long positions and pay more attention to risk control. Before the National Day holiday, it is recommended to reduce positions to avoid risks.

For queries and more information/data/reports access, please contact Paula Xu at xuzhongping@mysteel.com